Hydrogen’s anticipated role in road transport “has notably diminished”, according to a new report from Westwood Global Energy Group. It said progress in building a European renewable hydrogen industry has been limited, and it has been particularly slow in the UK.

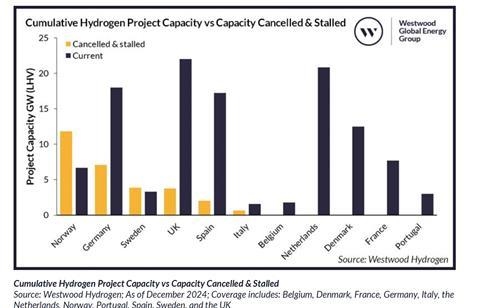

In its report, Europe’s Hydrogen Future: How Much Is Realistically Achievable? the group says a significant proportion of hydrogen production projects are stalled or cancelled. It said the industry’s slow growth is due to stringent regulatory frameworks and the cost gap between renewable, low-carbon and fossil-based hydrogen, “which has made securing long-term offtake agreements difficult”. These challenges have been “particularly evident across key sectors initially considered viable”, such as heating, road transport and export.

In road transport, hydrogen’s diminished role is reflected in closures such as H2Mobility shuttering over 25% of German hydrogen stations. H2Mobility’s strategy is to pivot towards commercial and heavy-duty vehicles, the report says, but, “Given the challenges hydrogen has faced, a critical question emerges of how much can realistically be achieved in Europe’s hydrogen market”.

In the UK, the Climate Change Committee (CCC) now predicts a predominantly battery electric road transport future for the UK by 2050, reserving hydrogen for niche applications such as construction and heavy industry equipment.

The report says the UK industry is still waiting for updates on the Hydrogen to Power Business Model (H2P BM), transmission-level gas grid blending and hydrogen heating strategies. Progress “has been impeded by significant bureaucratic hurdles and delays, lagging behind the EU’s evolved funding approach” and only three out of 11 hydrogen projects due to be backed by government have secured grants.

The report stresses the importance of demand-driven and offtake-focused mechanisms and “the critical need for clear end-use markets”. The EU has several demand-side mandates that will take effect by 2030, including road transport, that would require around 1 GW of dedicated electrolyser capacity. In contrast the UK has only one, which is in aviation, and does not explicitly require hydrogen use. “This disparity highlights a critical gap in the UK’s hydrogen strategy and a key area for policy development,” the report says.